What Compound Explained – What it Actually Is

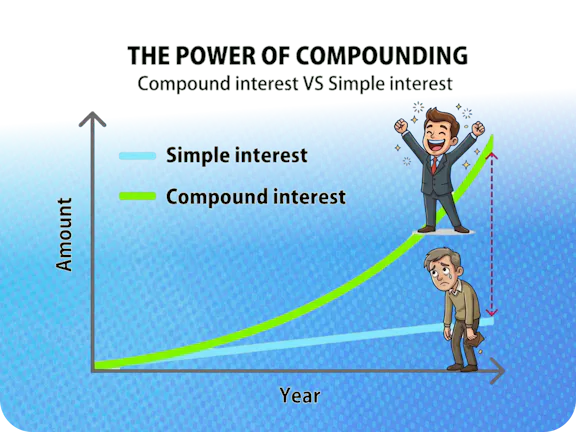

Regular interest is simple. You put in $100, earn 10%, get $10. Same every year.

Compound interest is different. You put in $100, earn 10%, get $10. But next year you earn 10% on $110, not $100. The year after that, 10% on $121. The interest earns interest. The pile keeps growing on itself.

That’s it. That’s the whole concept.

It sounds small at first. It isn’t. Over long periods it turns modest contributions into serious money without you doing anything extra. I started putting $150 a month into an index fund at 29. Nothing dramatic. I set it up, automated it, and forgot about it for three years. When I checked the balance I had contributed $5,400 and the account was worth $7,100. That $1,700 came from doing absolutely nothing.

Albert Einstein allegedly called it the eighth wonder of the world. Whether he actually said that is debated. Whether it’s true is not.

The Snowball in Real Numbers

Here is what $100 a month invested at 10% average annual return actually looks like:

- After 10 years: roughly $20,000

- After 20 years: roughly $76,000

- After 30 years: roughly $226,000

See also: The Rule of 72

You contributed $36,000 of your own money over 30 years. The rest — $190,000 — came from compound growth. You didn’t earn it by working harder. You earned it by starting early and leaving it alone.

Notice the curve. The first ten years feel slow. The second ten years pick up. The third ten years accelerate hard. This is the bend in the curve that changes everything.

The math rewards patience more than effort.

Now here’s the cost of waiting five years. If you start at 30 instead of 25 with the same $100 a month at 10%, you end up with around $150,000 at 65 instead of $226,000.

Starting your investment journey late, is it worth it?

Five years of delay cost you $76,000. That’s $76,000 for doing nothing differently except starting later.

Time is the ingredient nobody can buy more of.

How to Put It to Work Today

Compound interest only works if your money is in the right place.

It does not work in a checking account. It barely works in a standard savings account. It works in:

- A high yield savings account for your emergency fund

- An index fund inside a Roth IRA or 401(k) for long term money

- A taxable brokerage account for anything beyond that (Compare accounts)

The account matters because the rate matters. At 0.01% compounding does almost nothing. At 7% to 10% it builds serious wealth over time.

The other ingredient is automation. Set up an automatic transfer on payday — even $50 a month — into your investment account. You won’t miss money you never see. And consistency over time beats larger irregular contributions almost every time. Live below your means.

The one rule that covers everything:

Start small. Start now. Don’t stop.

Not when the market drops. Not when life gets expensive. Not when it feels like the amount is too small to matter. It always matters. The snowball needs time on the hill.