What a Roth IRA Actually Is

Whatis a Roth IRA? It is a retirement account with one unusual feature.

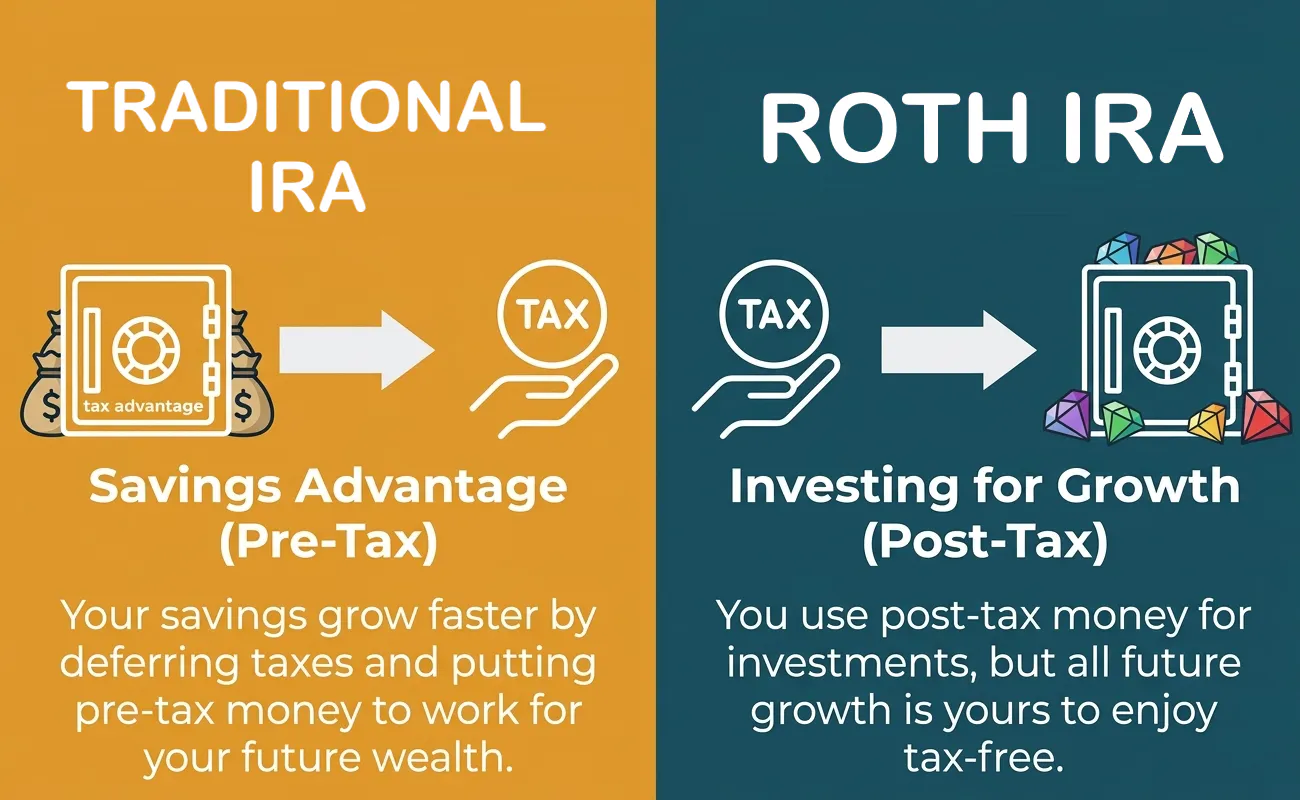

You pay tax on the money before it goes in. After that, it grows tax free. When you retire and take money out, you pay no tax on any of it — not on the original contributions and not on decades of growth.

With a regular retirement account, you get a tax break now but pay tax when you withdraw. With a Roth, you pay tax now and never pay again. Pair it with an index ETF inside.

Why does that matter? Because the growth is where the real money is. $6,000 invested at 25 could grow to $100,000 or more by retirement. With a Roth, that entire $100,000 is yours. With a traditional account, you owe tax on every dollar of it.

Young people benefit most from a Roth because they have the most time for tax free growth to compound. The earlier you start, the bigger the advantage.

The Numbers That Make It Powerful

In 2024 you can contribute up to $7,000 a year to a Roth IRA if you’re under 50. That’s about $583 a month. (Official IRS contribution limits)

You don’t have to contribute the maximum. Any amount helps.

I opened my Roth IRA at 31 and my only regret is not doing it at 21. I put in $50 a month to start because that was all I could manage. I remember thinking it was pointless at that amount. It wasn’t. That account is now one of my most valuable assets and it started with fifty dollars.

Here’s what $6,000 a year invested in a Roth IRA at 10% average return looks like:

- After 10 years: roughly $105,000 — all tax free

- After 20 years: roughly $378,000 — all tax free

- After 30 years: roughly $1,083,000 — all tax free

The power of compound interest.

In a taxable account you’d owe capital gains tax on the growth. In a traditional IRA you’d owe income tax on withdrawals. In a Roth, the government has no claim on any of it.

The difference between a Roth and a traditional IRA comes down to when you pay tax. If you expect to be in a higher tax bracket in retirement than you are now — which is likely if you’re young and early in your career — the Roth almost always wins.

See also: Starting late — is a Roth still worth it? & 401(k)

How to Open One This Week

Three brokerages make this easy: Fidelity, Vanguard, and Schwab. All three are free to open, well established, and beginner friendly.

Go to any one of their websites, click open a Roth IRA, and follow the steps. You’ll need your Social Security number, a bank account to fund it, and about fifteen minutes.

Once it’s open, put your contributions into a low cost index fund — VTI or VOO, the same ones covered in Article 6. The Roth IRA is just the container. The index fund is what goes inside it. That combination — Roth IRA plus index fund — is one of the most powerful long term wealth building tools available to ordinary people.

One rule most people miss: you must have earned income to contribute to a Roth IRA. You can’t contribute more than you earned that year. If you made $4,000 at a part time job, your maximum contribution is $4,000, not $7,000. This applies to students and part time workers especially.

Start with whatever you can. Even $50 a month inside a Roth IRA beats nothing by a significant margin over time.