The Number Your Bank Shows You Is Not the Whole Story

Your savings account says 4.5%. Looks decent. Feels responsible.

But that number is incomplete. It tells you what you earned. It does not tell you what you kept.

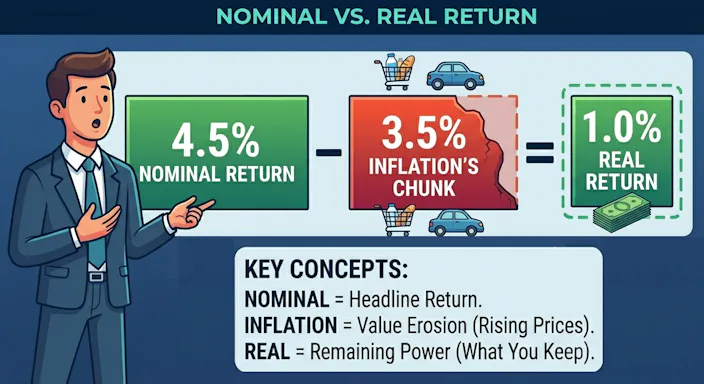

That 4.5% is called a nominal return. It’s the headline number, the one banks advertise, the one that shows up on your statement. It counts every dollar of interest you earned without accounting for what happened to the value of those dollars while you were earning them.

Inflation happened to them.

If prices rose 3.5% over the same period, your 4.5% account didn’t really earn you 4.5%. It earned you the difference. In this case, about 1%. That’s what actually stayed in your pocket in terms of real purchasing power.

The rest got eaten.

This applies to every return you will ever see. Every savings rate, every investment gain, every interest payment. The nominal number is just the starting point. The real number is what matters.

Most people never make this adjustment. They see 4.5% and feel good. The bank knows this. It’s easier to advertise a number that sounds better than it is.

I spent two years feeling good about a savings account paying 2.1%. Then someone asked me what inflation was running at that year. It was 4.2%. I had been celebrating a loss for 24 months without knowing it.

What a Real Return Actually Is

The formula is one step.

Real return = nominal return minus inflation rate.

Use the Rule of 72 to see the impact

That’s it. Subtract the inflation rate from whatever your account or investment is paying you. What’s left is your real return — the actual gain in purchasing power.

Some examples:

- Nominal return 4.5%, inflation 3% — real return is 1.5%

- Nominal return 2%, inflation 4% — real return is minus 2%

- Nominal return 10%, inflation 3% — real return is 7%

That second one is important. A 2% nominal return in a 4% inflation environment is not a small gain. It is a loss. Your money grew on paper and shrank in reality. Both things happened at the same time.

This is why the inflation rate is not just background noise on the evening news. It is the single most important number to hold next to any return you are earning. Without it, you are only seeing half the picture.

A positive real return means you gained purchasing power. You can buy more with your money than you could before.

A negative real return means you lost purchasing power. You can buy less, even if your balance went up.

The goal of any savings or investment decision is a positive real return. Everything else is just a slower way of falling behind.

Real World Examples That Hit Close to Home – Real return vs Nominal Return

Let’s make this concrete.

Say you had $10,000 at the start of last year and inflation ran at 3.5%.

Here is what each common option actually returned in real terms:

Standard checking account at 0.01%

Nominal gain: $1. Real return: minus 3.49%. You lost $349 in purchasing power while your balance barely moved.

Big bank savings account at 0.5%

Nominal gain: $50. Real return: minus 3%. You lost $300 in purchasing power after your interest is factored in.

High yield savings account at 4.5%

Nominal gain: $450. Real return: plus 1%. You kept $100 of real purchasing power. Not life changing but you moved forward.

S&P 500 index fund at 10% average (historical returns)

Nominal gain: $1,000. Real return: plus 6.5%. You kept $650 of real purchasing power. Over time this compounds into something significant.

The gap between the checking account and the index fund is not just $999 in nominal terms. It’s the difference between losing $349 and gaining $650 in real terms. That’s a $999 swing in purchasing power from a single decision about where to put your money.

Same $10,000. Four different outcomes. One variable: where you put it.

Why This Changes How You Should Think About Every Financial Decision

Once you see returns in real terms, you can’t unsee it.

Every financial decision has a real return attached to it. Not just savings accounts and investments. Debt too.

If you have a credit card charging you 22% interest, that debt has a real cost of roughly 19% in a 3% inflation environment. Paying it off is the equivalent of earning a guaranteed 19% real return. No index fund, no savings account, nothing available to a regular person beats that.

See also: Should you pay off debt or invest first?

This is why high interest debt is always the first priority. The real return on eliminating it is higher than almost any investment you could make.

On the flip side, a low interest mortgage at 3% in a 4% inflation environment has a negative real cost. Inflation is actually reducing the real value of your debt over time. In that case, investing surplus cash rather than aggressively paying down the mortgage can make more sense in real return terms.

Before you put money anywhere, ask one question.

What is the real return on this decision?

Savings account, investment, debt payoff, or even a big purchase — run the real return calculation first. It won’t always give you a clean answer but it will always give you a clearer one.

That one habit separates people who build wealth slowly and steadily from people who work hard their whole lives and wonder where it all went.

Compound interest explained